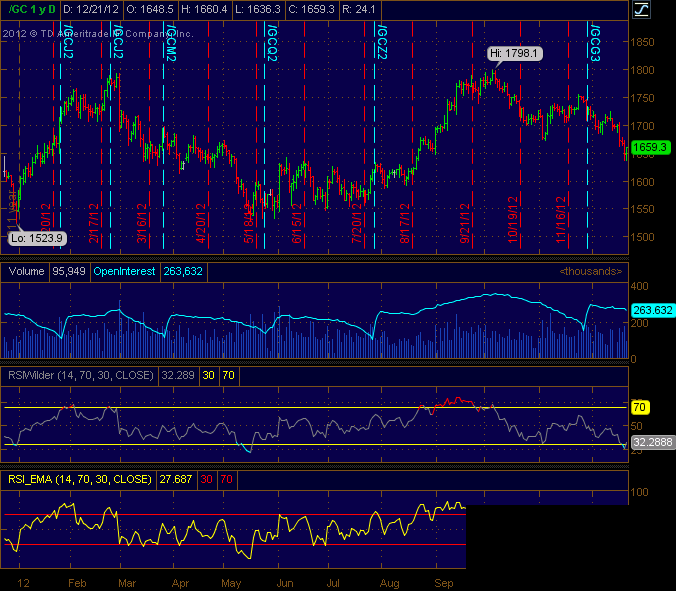

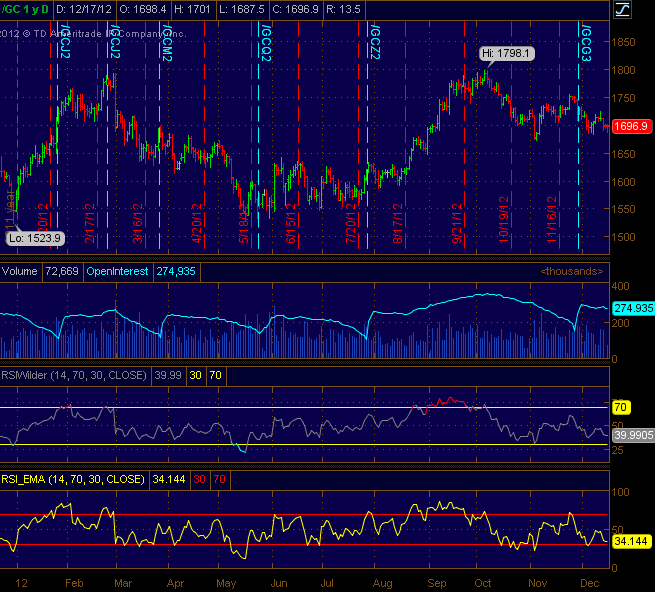

Traders have been bearish on gold and gold stocks since late October, the longest stretch in recent years. All such previous instances were followed by significant multi-week rallies. Here’s a daily chart, showing some divergence in RSI.

Here is GDX, the gold miner ETF, which looks good technically, as well as being cheap vs. the metal itself:

A caveat here is exemplified by the coffee futures market (see recent posts), which has steadily declined since a manic high 18 months ago. Gold and silver experienced a mania around the same time, which perhaps capped their 11+ year bull run. If that is the case, a situation like the present could actually resolve not in a rally, but in a crash, as crashes may develop from oversold and bearish conditions that would otherwise be bullish. For this reason, as well as the value discussion below, I would be careful about any longs and use a stop-loss.

I still maintain that gold is overvalued relative to a meaningful basket of other assets and metrics. Today, a kilo of gold buys (or rents) you more real estate, commodities, labor, automobile, etc. than at any time in modern history, save bottoms in those respective markets and tops in the metal.

This doesn’t mean that gold can’t rally for a few weeks or months or even make a new high – it just means that doing so would make it even more historically overvalued. The time of gold being a great value has long passed. It has done a very nice job at protecting holders against the Federal Reserve’s war on savings, just like it did a good job at protecting against inflation in the late 1970s, but gold peaked prior to inflation, and today gold may peak prior to the end of Bernanke’s tenure.

I often make the point that gold is not the only hard asset. In an inflationary episode, there are many ways to play. The dollar lost 2/3 of its value from 1980 to 2000, but over that period gold lost 90% of its value when adjusted for inflation (70% nominally). As in equity investing, the price you pay determines your return. I would look for hard assets that are closer to historical lows, or at least mean values, rather than something near a high. Distressed real estate comes to mind, or even Japanese equities.

Heck, if we get another cyclical equity bear market within the post-2000 secular bear, there will be plenty of hard, productive assets available for reasonable prices in the stock market. BTW, every episode of double-digit inflation in the US since 1900 has ocurred during the latter years of a secular bear market in equities (1919-1920, early 1940s, 1979-1982). Thanks in large part to Mish‘s explanations of the credit market, I have been a deflationist since late 2007, despite the shrill warnings of the hyperinflation crowd. There is no telling how long our own Japanese situation lasts, but we likely have at least a couple more years to go.