Jump to 1:05 for the action.

Who says small dogs are no fun?

Reply

Jump to 1:05 for the action.

From Mish:

The German 30 year bond is yielding 2.8%:

bloomberg.com

The US 30 year bond is yielding the same:

Yahoo Finance

There is no margin of safety in Germany debt against the strong likelihood that the country will be forced (by Merkel and other banker tools) to absorb the losses of the rest of Europe.

Of course, there is no margin in safety in US bonds either at this price, certainly not enough to compensate for the probability of trillion dollar deficits forever. I expect yields to stay low through this cyclical bear market, but not much beyond that. Bonds will continue to be a good short at times when they are overbought, and we may be approaching such a time.

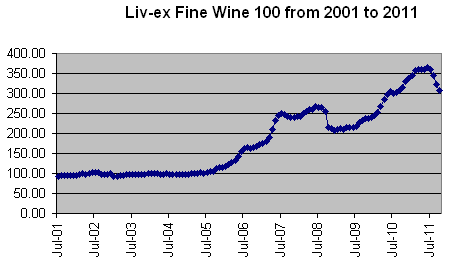

Here’s the 10-year chart, created from data provided by liv-ex.com:

Wine investing is a silly fad, since very few wines improve beyond a few years (this index does not track the same bottles – it’s components are continuosly updated). Most wines are undrinkable after 10-25 years, with exceptions like a few sweet wines such as Tokaji and Eisweins, in which the sugar acts as a preservative (5000 y/o Egyptian honey is still good). How is an amateur to know when to sell a wine before it expires, or even find a buyer for such an illiquid asset? I suspect that most new investors aren’t even aware that even very expensive wines can expire virtually worthless. A few sharpies in France and California may be making a lot of dough off newbies.

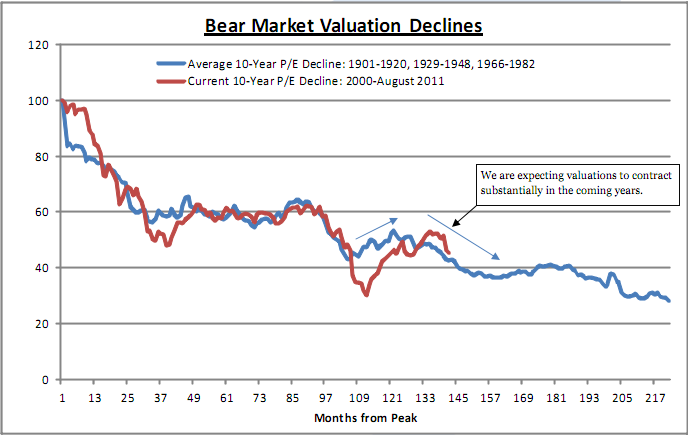

Mish Shedlock’s investment management company, Sitka Pacific, provided this chart in their September letter (as a non-client, I only get delayed copies):

-

One lesson to be learned here, which they get into in the letter, is that prices bottom before valuation multiples. In the bears of the 1910s, ’29-early 40s and ’66-82, inflation appeared late in the game. BTW, this meshes with Kondratieff theory, where inflation leads to disinflation to deflation then inflation again, with asset values moving in tandem.

So, be prepared to buy in this coming wave down, if we get a nice drop over the next year or so, because select equities could be a nice hard asset to own through the turmoil in the currency and sovereign debt markets, which is likely to spread to the US, UK, Germany and Japan by later this decade.

Today’s ad-hoc explanation of market action seems to be the failure of the US Congress’ “supercommittee” to come up with a deal to slightly shrink the 2nd derivative of budget growth over 10 years. What a joke! Europe was down over 3.5% today – does anyone there know or care about the supercommittee? What about the Russians (-5%) or traders in Hong Kong last night (-1.5%)? There is a deficit of over a trillion dollars a year, and this committe was talking about spending a trillion less over 10 years than they would at the current pace of growth, as if Congress ever sticks to previous budget plans anyway.

Nobody but journalists has cared about this noise, since it is clear that Congress and the executive will do nothing to meaningfully address the budget gap until the bond market forces their action. If we are in another strong wave down in the secular (post-2000) bear market, this will buy the government (and probably those of Japan, Germany, France and the UK) another year or more before interest rates start to creep higher and force defaults and spending cuts. This outcome is inevitable, since the welfare state Ponzi schemes must collapse and screw the later generations of entrants, as in all Ponzis.

So why is the market down today? Because we’re in a bear market, and Oct-early Nov relieved the oversold condition that had built up by the end of September (lowest, longest-sustained DSI bullishness since 2009). Since before it started, I have viewed this rally aspossibly similar to what we experienced from mid-March to late-May 2008. If the corollary holds, we will be back under SPX 1100 by the New Year.

Journalists are lazy and make up explanations for market action without any empirical evidence, always assuming that correlation equals causation. If every day you magically had the next day’s news headlines, I doubt it would offer much if any trading advantage.

From his Texas Straight Talk column on his Congressional site:

This week marks the deadline for the so-called congressional Super Committee to meet its goal of cutting a laughably small amount of federal spending over the next decade. In fact the Committee merely needs to cut about $120 billion annually from the federal budget over the next 10 years to meet its modest goals, but even this paltry amount has produced hand-wringing and hysteria on Capitol Hill. This is only cutting proposed increases. It has nothing to do with actually cutting anything. This shows how unserious politicians are about our very serious debt problems.

To be fair, however, in one sense members of the Super Committee face an impossible task. They must, in effect, cut government spending without first addressing the role of government in our society. They must continue to insist the federal government can provide Social Security, Medicare, and Medicaid benefits in the future as promised, while maintaining our wildly interventionist foreign policy. Yet everyone knows this is a lie.

Keep in mind that the 2011 federal deficit alone was about $1.3 trillion, which means the Super Committee needs to cut that much PER YEAR rather than over a 10 year period. If Congress ever hopes to address its debt problem, it must first stop accumulating any new debt immediately, in 2012.

Federal revenue likely will be about $2.3 trillion in fiscal 2012. The 2004 federal budget was about $2.3 trillion. So Congress simply needs to adopt the 2004 budget next year and the federal government will balance outlays and revenue. That’s all it would take to produce a balanced budget right now. Was the federal government really too small just 7 years ago, in 2004? Of course not. Only Washington hysteria would have us believe otherwise.

Read the whole thing here: http://paul.house.gov/index.php?option=com_content&task=view&id=1928&Itemid=69

It may be interesting to look at some of the public companies in the hardest-hit European countries, since the stock indices here are lower than anytime in at least a decade. Here are the results of a search for Greek shares, with an eye towards companies in defensive industries that will not be hurt, or could even benefit from a weaker currency.

All of these businesses are likely to survive a very bad economy, even if they go bankrupt – the question is how the equity holders will fare.

Athex index chart (Athex is now 60% lower than at the 2009 bottom): http://www.bloomberg.com/quote/FTASE:IND/chart

List of top 20 Greek companies by market cap as of May 2010: http://topforeignstocks.com/2010/05/09/the-top-20-greek-companies-by-market-capitalization/

Here are a few names – these first 2 look strongest to me (bottler and utility):

Coca Cola Hellenic Bottling Co:

Biggest foriegn Coke bottler

http://www.bloomberg.com/quote/EEEK:GA/chart

http://en.wikipedia.org/wiki/Coca-Cola_Hellenic

EUR 13.00, EPS 0.93 – not really cheap yet by earnings, 1.62x book. Keep an eye on this one.

Public Power Corp SA , ticker PPC

Biggest utility in Greece. To raise cash, the gov sold 17% of its until then 51% stake.

Plants are mostly coal-fired.

http://www.bloomberg.com/quote/PPC:GA

http://en.wikipedia.org/wiki/Public_Power_Corporation_of_Greece

EUR 5.30, EPS 1.10 – very cheap by earnings, 15% dividend yield.

Hellenic Telecommunications Organization S.A., ticker HTO

http://www.bloomberg.com/quote/HTO:GA

http://en.wikipedia.org/wiki/OTE

3.6% div yield, 15 PE. 1.14x book – not cheap at all, though stock is way down

Boutaris J & Sons Holdings SA , ticker MPK (preferred shares also traded)

6 Greek wineries, one in France, most recognised Greek wine brand

Company website: http://www.boutari.gr/?TEFORz1FTg==

http://www.bloomberg.com/quote/MPK:GA

No earnings data available, but trading at 0.3x book and 0.27x sales.

Attica Group

Largest ferry operator

http://www.bloomberg.com/apps/quote?ticker=ATTICA:GA

http://en.wikipedia.org/wiki/Attica_Group

No earnings data, but 0.12x book

ANEK Lines SA

Ferries

This is Nigel Farage, a UK delegate to the European Parlaiment, saying that all Europe really needs is free trade and some basic standards for regulation, not the whole mess of regulation and loss of sovereignty offered by Brussels today. (I totally agree about free trade, but where do you draw the line with labor and environmental regulation – so many of the EU’s silly laws today are in those spheres – better to just say, “Tarriffs, quotas and bans are hereby abolished within the EU. Fin.”).

It seems as though opinion within every EU nation is turning against the institution. This is good, but also dangerous, as it would be a shame to see Europe return to the mess of trade and travel restrictions that existed a few decades ago. The lack of such restrictions was a great contributor to the flourishing of civilization on that continent in the 19th century, and their reinstitution in the early 20th brought war. “When goods don’t gross borders, armies will.” -Frederic Bastiat

To everyone else in the western world, November 11 is Armistice Day or Remembrance Day, a day to contemplate the lessons from and the ending of the Great War. WWI of course destroyed Europe, setting the stage for fascism and communism, and ended the longest and fastest period of economic growth and improvement in living standards in modern history.

In America, today is Veterans’ Day, and we are expected to celebrate soldiering and pretend that the wars into which politicians have thrown our young men have all been for our benefit, specifically the protection of our freedoms. It’s just another opportunity to beat the drums, like staging a ballgame on the deck of an aircraft carrier.